According to the latest news on the 19th, Acacia Partners, a US hedge fund that is one of the major shareholders of Baidu, recently stated in an open letter to Baidu’s chairman and CEO, Li Yanhong, that the IQI’s 2.8 billion US dollar valuation is too low. The interests of Baidu and its shareholders demanded the cancellation of the ongoing privatization of Iqiyi.

To understand exactly what Acacia Partners is against, it has to start with the iQIYI itself.

Iqiyi is a streaming media website based on online video. Its cost mainly comes from copyright outsourcing and home-made content, as well as network server transmission storage and encoding processing. The main source of income is advertising, membership dues and copyright distribution, but also a small amount of iQIYI games and e-commerce revenue.

As we all know, in the current domestic environment, this type of network streaming media platform must have much lower income than expenditure. It is entirely dependent on the backing giants to survive, such as Youli behind the potatoes, Tencent behind the Tencent video.

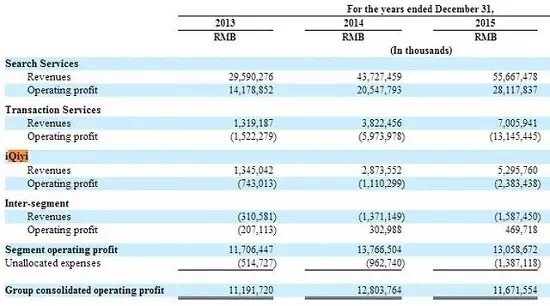

Of course, there are giants behind iQIYI. Since August 2011, Baidu has subscribed for iQiyi B round of preferred stock for $45 million. At present, Baidu already owns up to 80.5% of iQiyi. However, as the top spot in the domestic video streaming media business, iQiyi’s continuous high-cost burning model has caused its loss amount to continuously expand in the last three years. The data shows that from 2013 to 2015, the losses of iQIYI reached 743 million yuan, 1.11 billion yuan and 2.38 billion yuan respectively.

This also affects the controlling Baidu. According to Baidu's third-quarter earnings report in 2015, Baidu’s operating profit was only RMB 2.512 billion, a drop of 35.9% year-on-year, and the biggest reason was the immense investment in iQiyi. Baidu insiders said that in the third quarter of 2015, iQIYI lowered Baidu's operating margin by 5.4 percentage points.

Therefore, Baidu has always wanted to get rid of iQiyi this financial report burden, and instead use a more cost-effective way to join this "video war", for example, Baidu's "Go to where the network" and "Baidu takeaway" approach is an option.

So, in February of this year, Baidu announced that Li Yanhong and Igyi’s CEO Gong Yu will acquire the 80.5% stake in iQiyi held by Baidu at a valuation of RMB 2.8 billion. If the transaction is successful, iQIYI will Separation from Baidu assets, indirect privatization. After the privatization, iQIYI can follow the trend to achieve the split of the VIE structure, and then turn to the domestic market for listing, seek capital support in the open market, and supplement the "ammunition" required for the burning mode.

At the time, Gong Yu issued an internal letter saying that privatization was "to gain more support from the Chinese market and to obtain stronger financing capabilities." He said that after the completion of privatization, iQiyi will seek domestic listing at the right time.

Today’s latest news shows that Baidu’s major shareholder, Acacia Partners, apparently opposed 2.8 billion valuations and privatizations.

In a letter to Li Yanhong, Acacia Partners stated that the valuation of iqiyi’s $2.8 billion was too low, which seriously damaged the interests of Baidu and Baidu shareholders. The open letter stated: "Although the sale of iQIYI can improve Baidu's profitability in the short term, the immediate interest compared with the long-term potential value that Baidu retains for iBeiyi's shareholders is insignificant." The investment in iQiyi in the past two quarters is “a huge gift from current Baidu shareholders to future iQiyi shareholdersâ€.

Acacia Partners believes that iQiyi is China's leading video site, and its $2.8 billion valuation is too low. The statement quoted the report of an independent research organization 86Research on May 2 this year as saying that the valuation of iqiyi should be set at US$5.8 billion, which is more than twice that of US$2.8 billion. In addition, referring to the second half of last year, Alibaba.com acquired the major competitor Youku of Iqiyi for US$4.8 billion, and the company’s performance was somewhat lower than that of iQiyi. From this point, it can also be seen that 2.8 billion yuan. Is a relatively low valuation.

The following is the full text of the open letter:

Dear Mr. Li Yanhong,

Hello!

We hereby send a letter to Baidu’s shareholder. Since September 2012, we are the Baidu shareholder and currently hold more than 2.6 million Baidu American depositary shares, valued at more than US$400 million. Our typical investment period will exceed seven years. We have always appreciated your management and operating capabilities. We admire that you can lead Baidu from a start-up company to become the industry leader today, so we hope to hold Baidu shares for a longer period of time. An early member of Baidu’s board of directors once told us that “Yanhong is regarded Baidu as its own childâ€. This is indeed the case. During the past eleven years of Baidu’s listing, we have also witnessed your love for Baidu’s growth and the integrity it has displayed in the process. Just as we are nurturing children, we hope that we can also do it. To the same.

It is also because of your understanding of Baidu's efforts, we are surprised and puzzled by your proposed privatization and acquisition of iQi. We are convinced that your proposal to acquire iQiyi is contrary to the long-term benefits of Baidu and its shareholders. The reasons are as follows:

1. We believe that although selling iQIYI to you can increase Baidu's profitability in the short term, the immediate interest is insignificant compared to the long-term potential value that Baidu has retained for iBeiyi.

2. We think your valuation of iQIYI is too low.

3. We are concerned that Baidu’s vigorous investment in iQiyi in the previous quarter will be a huge gift to Baidu shareholders for the future iQiyi shareholders (including you and the acquisition partner). We are worried that making a decision with an inherent conflict of interest will undermine your reputation with Baidu. Baidu should be a respected and important company, not a cash-out tool for personal economic benefits.

(Finish)

In May, Lenovo also announced that it would backdoor A-share listings in 2017, but it was later officially denied. It seems that the privatization of iQiyi is destined to not be easy.